Unitary taxation: What would formulary apportionment mean for countries and multinationals?

- Read this in:

- en

Table of contents

This blog outlines the key findings from a new study on unitary taxation and formulary apportionment. You can read the simplified press release here. Readers interested in diving deeper into the data can explore the charts, country-level results, and methodological notes on our separate data and visualisations page.

Key messages from this study

Unitary taxation tackles profit shifting by taxing multinationals where they have real jobs, sales, and assets, rather than where they book profits on paper. This shift increases the tax base for most countries, with the exception of pure tax havens.

When more weight is given to employment factor when determining taxing rights, labour-intensive economies gain more, giving the Global South a fairer share of revenues

High-income, capital-exporting countries are not left behind; major economies including the US, Germany, the UK, and Australia often record gains, particularly when a strong global minimum tax is in place.

Jurisdictions that rely heavily on artificial profit booking lose out, but those with some real activity, like Ireland or Switzerland, can retain revenues if they raise effective rates and ensure genuine economic substance.

Most multinationals would see only modest increases in their tax bills, with sharper rises concentrated among the most aggressive profit shifters.

1/ Introduction: A fairer way to tax multinationals

Across the global labour movement, pressure has been growing to fix the international tax system and to ensure multinationals are taxed where real economic activity takes place. At the heart of this call is a shift away from the flawed “separate accounting” model, which treats each subsidiary as a standalone entity and allows profits to be booked in low-tax jurisdictions, far from where value is created. In its place, unions and tax justice advocates have long argued for unitary taxation with formula apportionment. This system would tax multinationals as single, unified firms, and allocate their global profits based on indicators like employment, assets, and sales.

This approach is not new. It’s long been used within federal systems like the United States, Canada, Germany, and in Japan. In the EU, a variant was proposed under the Common Consolidated Corporate Tax Base (CCCTB) and is now being revisited through BEFIT. Globally, elements of unitary taxation have also entered the OECD’s Pillar One proposal, which introduces limited profit reallocation based on sales destination and signals a shift in international thinking.

This study builds on those well-established developments. Commissioned by the Network of Unions for Tax Justice (NUTJ) and the Austrian Chamber of Labour, it presents the most comprehensive modelling to date of what a global shift to unitary taxation could mean: for governments seeking revenue, for workers in countries that currently lose out, and for multinationals facing a reallocation of tax liabilities. The research was carried out independently by Professor Simon Loretz (Senior Economist at WIFO, the Austrian Institute of Economic Research), with guidance from a reference group of trade union representatives and tax experts. It covers over 7,400 multinational groups across 161 jurisdictions, offering an unprecedented view of how taxing rights would shift under different scenarios.

For more tax justice briefs from the NUTJ, check out the key resouces page.

Understanding the dataThis study combines several sources to model how unitary taxation would affect countries and multinational groups:

To allocate profits, the study uses several “weighted formulas” that split taxing rights across sales, jobs, and assets in different proportions:

In this blog, results are shown mainly using the Double Sales weighted formula, because it best illustrates a balanced outcome. Where relevant, we also provide ranges based on CCCTB to show how results vary across weighted formulas. |

2/ How taxing rights would be redistributed

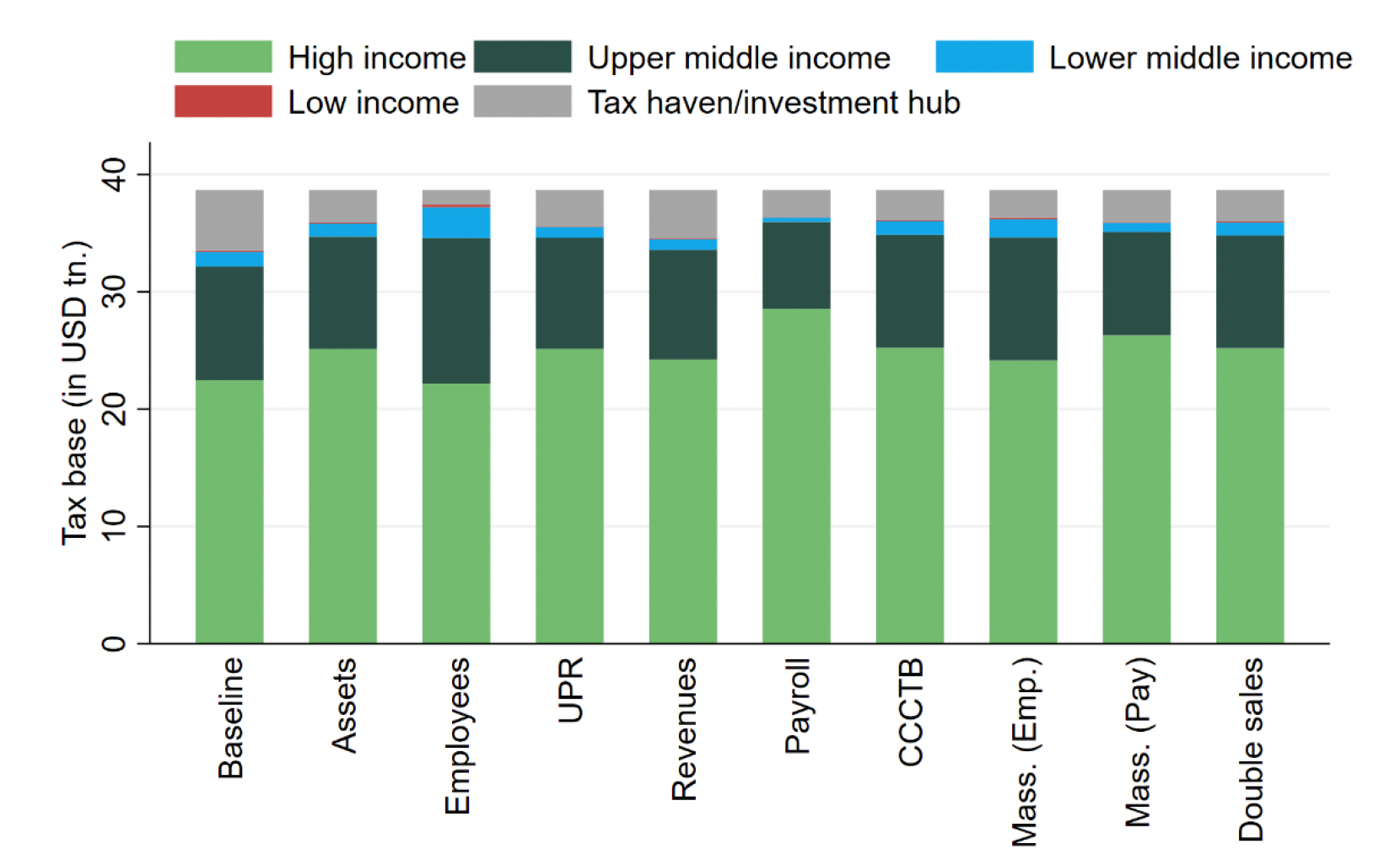

Tax havens and low-tax countries are the biggest losers under any formula

The clearest trend is that tax havens would see dramatic reductions in their share of the global corporate tax base. Smaller jurisdictions like Bermuda or the Cayman Islands risk losing 80–90% of their tax base under most apportionment scenarios, which is a direct result of booking high profits with little real activity. Financial centres such as Luxembourg, Switzerland, and the Netherlands also face consistent losses, since much of the profit they attract reflects tax planning rather than production or sales. For these jurisdictions, the findings underline the fragility of models built on paper profits, and the need to reflect on more sustainable strategies rooted in real economic activity and resilience.

Employment-based formulas shift taxing rights toward labour-intensive economies

Including employment in the apportionment formula helps correct a core imbalance: countries whose workers generate value capture a fairer share of taxing rights, rather than revenues ending up in tax havens or residence countries. This would provide important fiscal space for national development, since many labour-intensive and lower-income economies rely proportionally more on corporate income tax than high-income countries.

The distributional effects are clearest under a single-factor employee headcount scenario. India’s tax base more than doubles, while Indonesia and Brazil record gains of over 40% each, reflecting their large, but under-recognised, role in global value chains. Simulating only the cost of employment (payroll), by contrast, favours high-wage economies: France’s tax base rises by 68%, Germany’s by 66%, Canada’s by 61%, and the UK’s by 48%. In practice, the choice is unlikely to be one or the other. A mixed formula, such as the double sales model, is the most likely outcome, offering a balance between the two.

Balanced formulas still beneficial to high-tax industrial countries

When profits are apportioned using balanced “weighted” formulas such as Double Sales (which gives half the weight to sales, a quarter to assets, and smaller shares to jobs) and CCCTB (which places roughly equal weight on sales and assets, with smaller shares for headcount and payroll), large, high-tax economies continue to benefit. Belgium’s tax base increases by 81-84%, with the sharp rise partly due to the redistribution of large reported losses from Luxembourg, showing how spillover effects from neighbouring jurisdictions shape results. Romania records gains of 43-50%, France gains 33-35%, Italy’s increase is around 26-28%, Spain rises by 27-29%, and Australia gains 17-19%. The United States records a 19% increase under Double Sales, with slightly higher gains under other payroll-heavy formulas. These outcomes highlight how weighting sales and real activities redistributes taxing rights back toward larger, high-tax industrial economies.

Concerns from capital-exporting countries may be overstated

A common assumption in international tax debates is that high-income, capital-exporting countries would be disadvantaged under a unitary taxation system. But the picture is more mixed. Germany consistently gains, with increases of 25% under Double Sales and 27% under CCCTB. Japan’s tax base falls modestly, by 7-8% depending on the formula. China records a smaller reduction of around 4 %, while Norway sees larger declines of 14-15 %. These shifts reflect differences in each country’s economic structure, with those hosting higher domestic demand, wage costs, and employment faring better under formulas that weight sales and payroll.

Concerns that higher corporate tax burdens could undermine investment or employment are not borne out in the evidence. A 2025 global study by Agustina Gallardo shows no systematic link between stronger corporate taxation and weaker labour markets. On the contrary, countries with robust corporate tax systems tend to record stronger formal employment, fairer wage distribution, and better-resourced public services.

Importantly, even where tax base allocations shrink, countries can still increase their overall tax revenues by raising effective tax rates. As the research shows, applying a robust global minimum corporate tax, such as the 25% scenario the study modelled, boosts revenues significantly across nearly all country groups. For some countries that would otherwise lose out under unitary taxation alone, like Ireland, the minimum tax is decisive: revenues fall slightly under unitary taxation, but more than double when the 25% floor is applied. This makes the reform more fiscally viable for countries with small base reductions.

Most tax base remains in higher-income countries — but the system becomes fairer

Despite these redistributions, high- and upper-middle-income countries still retain the majority of the global tax base under all scenarios. This reflects the fact that most economic activity remains concentrated in these economies. What unitary taxation changes most is not so much the overall size of the tax base, which may shrink by around 6-10 % due to international loss consolidation, but who has the right to tax it.

Figure 1. CBCR data -Tax base allocation, by apportionment factors, by country groups

Source: 1 OECD and author's estimations. Based on aggregated CbCR data, sums 2016-2021.

The first bar (“Baseline”) shows the distribution of the tax base under the current separate accounting system, while the other bars show simulated allocations under different unitary taxation formulas.

3/ The revenue effects of unitary taxation

Revenue outcomes depend heavily on tax rate assumptions

Redistributing tax bases is only half the story. Whether countries gain or lose tax revenue under a unitary system also depends on what tax rates are applied to those profits. To explore this, the study models three different tax rate scenarios: i) one where each country applies its statutory corporate tax rate, ii) another based on effective tax rates (closer to what multinationals actually pay today) and iii) finally one in which a 25% global minimum tax is introduced.

Statutory rates show the upper bound of potential revenues

Applying statutory rates to a unitary system produces striking results: global revenues rise by more than 40%, from $7.3 trillion to over $10.3 trillion (2016–2021 totals).

High-income countries capture most of this gain, increasing collections by about 64% under both CCCTB and Double Sales.

Upper-middle-income countries see more modest increases of around 11-12% while lower-middle and low-income countries actually record declines of around 12% and 27% respectively. These losses reflect the relatively low weighting of employment headcount in the double sales formula, which disadvantages labour-intensive economies.

Tax havens and investment hubs appear to gain between 14-20%, but this is concentrated in larger hubs with real activity such as Ireland and Switzerland. Smaller pure havens with little economic substance, such as Bermuda or the Cayman Islands, lose 80–90% of their tax base across formulas, leaving little scope for meaningful revenues.

Yet these statutory-based results are theoretical as no country actually applies headline rates across all profits. Some deviations are legitimate, such as credits for job creation or industrial policy. Others are much harder to defend, notably preferential regimes like patent boxes that allow certain income to be taxed far below headline rates. Because the simulation assumes full statutory taxation without accounting for these carve-outs, it likely overstates what governments could actually raise.

Effective tax rates provide a more realistic picture

When ETRs are applied to the unitary simulation, global revenues fall slightly, around 5% below the current baseline. But the distribution of taxing rights shifts more fairly.

Tax havens see revenues fall by about one-third, from around $409 billion to $229–240 billion depending on the formula, as inflated profit shares disappear.

High-income countries remain within about 3.6% of their current levels under both CCCTB and Double Sales, suggesting resilience under most formulas.

For lower- and middle-income economies the results are mixed. Labour-intensive countries such as India, Indonesia, and Brazil fare better under headcount-based formulas, while others see declines of 10–20% without complementary reforms.

Taken together, the statutory and ETR simulations highlight the size of the gap created by special regimes. The key policy task is to narrow that gap by removing wasteful incentives while keeping those with a clear public purpose, so that effective rates move closer to statutory levels.

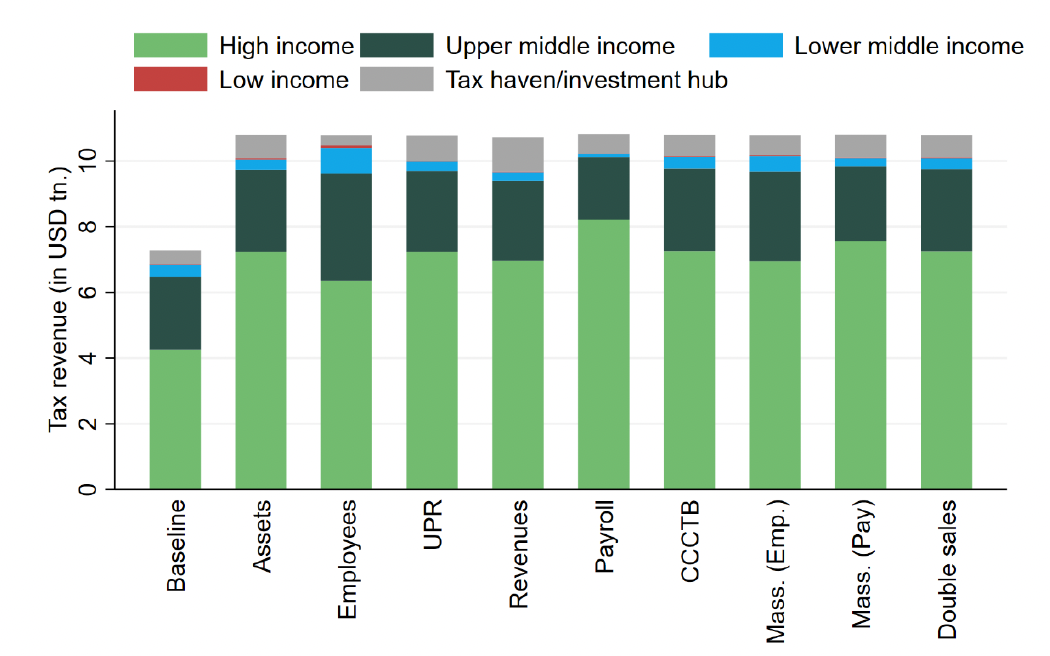

A 25% global minimum tax boosts revenues while limiting inequality

One way to close the gap between statutory potential and current effective collections is through coordinated minimum taxation. The study models what happens if a 25% global minimum corporate tax is introduced on top of unitary taxation. This brings global tax revenues to their highest level — over $10.7 trillion, nearly 50% more than under current rules. This scenario combines the effect of profit reallocation with a backstop that prevents profits from slipping through the cracks.

Using balanced formulas such as Double Sales and CCCTB, the results show:

High-income countries see revenues grow by almost 70%, rising from $4.27 trillion to $7.25–7.26 trillion depending on the formula.

Upper middle-income countries record a 13-14% increase, rising from $2.2 trillion to around $2.49 trillion.

However, results are more mixed for lower-income countries. Revenues in lower middle-income and low-income groups fall by 5–10% and 16–26% respectively, reflecting the relatively lower weight on employment headcount, which can understate the contributions of labour-intensive economies.

These findings don’t diminish the potential of a global minimum tax, but they do show that design matters. Too often, international debates have been stuck in a sterile “for or against” discussion of formulary apportionment. What is needed instead are constructive assessments of how different formulas and tax rates play out in practice, and what adjustments could ensure fairer outcomes. Pairing strong minimum rates with formulas that better reflect employment and production can help ensure lower-income and labour-intensive economies also share in the gains. With careful calibration, the global tax system can both raise more revenue and distribute it more fairly.

Figure 2. Tax revenues by apportionment factors and country groups - estimations based on a minimum 25% global CIT rate

Source: 2 OECD and author's estimations. Based on aggregated CbCR data, sums 2016-2021

“The first bar (‘Baseline’) shows revenues under the current separate accounting system. The following bars show estimated revenues if countries applied statutory corporate tax rates to apportioned profits, with a 25% minimum rate applying where statutory rates are lower.

4/ What would change for multinationals?

Most multinational groups would face moderate increases in tax liabilities

When applying statutory tax rates, 57% of MNEs in the study would face an increase in tax liabilities. Across the full sample of 7,350 firms, the average increases range from 8.7% to 10.1%, depending on the apportionment formula, with the largest rises seen under sales by destination. However, the median increase is only 1.5%, reflecting the fact that while some firms face sharp rises, most experience limited change while a smaller subset, often those relying most heavily on profit shifting, would face sharper rises.

For the 6,983 MNEs already reporting positive tax liabilities, the average increase is more modest, between 3.7% and 4.9%, with a median of 4%. This subset provides a more meaningful indication of expected changes for firms currently subject to tax. Differences between formulas are relatively small, though apportioning profits based on sales by destination consistently results in the highest increases, and unrelated party revenues in the lowest.

Importantly, the hybrid data approach shows that these tax increases are mostly marginal, concentrated among MNEs engaging in aggressive profit shifting. Firms already paying close to their statutory rates see little change, while those funnelling profits through low-tax hubs are the ones most affected. This suggests that the shift to unitary taxation need not be highly disruptive, as most firms would see only marginal changes —reinforcing that the reform is not about taxing more, but taxing more fairly.

With a 25% minimum tax, tax increases become more widespread

In this scenario, about 61.5% of MNEs would see an increase in their overall tax liability. For those already paying tax, average increases are close to 8%, with a median of 8.5%. The differences between apportionment formulas narrow significantly when all profits are taxed at or above 25%, suggesting that global rate coordination reduces the scope for strategic tax planning.

The effect also broadens the pool of firms affected: even companies with less aggressive tax planning face some increases as low-tax jurisdictions are neutralised. Yet the largest jumps still fall on MNEs that had previously shifted substantial profits offshore, showing that the minimum tax mainly curbs the gains of habitual profit shifters while levelling the playing field for others.

Accounting for loss consolidation

In practice, unitary taxation includes international loss consolidation, meaning that losses in one country offset profits elsewhere within the same multinational group. This effect wasn’t modelled in the hybrid dataset used here, which means the increases in liabilities may be slightly overstated. The study estimates that full international loss consolidation would reduce the total tax base by 6–10%, especially in the early years of reform or during downturns. Even after accounting for loss consolidation, most profitable MNEs would still face higher tax bills than today, though many could use accumulated losses in the short term to soften these increases.

5/ What does this mean for labour and tax justice?

Unitary taxation would reduce incentives to offshore and reward real economic activity

By aligning taxing rights with where multinationals employ people, produce goods, and make sales, unitary taxation cuts down on profit shifting and encourages firms to maintain real operations. It reduces the incentive to offshore jobs and helps governments protect employment and domestic tax bases: a clear win for workers.

Crucially, this also means that governments in the countries where real activity takes place regain the revenues linked to that activity. This restored fiscal space can be used to support wages in the public sector, fund infrastructure, and expand social protections. These are benefits that flow back to workers and communities.

The report also notes there is little evidence that linking tax liabilities to employment would trigger widespread offshoring of labour-intensive activities. Experience from US states using formulary apportionment shows no significant negative impact on overall employment. Relocating real workforces is far costlier than shifting profits on paper, which helps explain why unitary taxation is more likely to stabilise jobs than threaten them.

Union experience reinforces this picture. Firms that engage most aggressively in tax avoidance rarely reinvest the savings in jobs or productive capacity, and often show weaker social dialogue with workers. Evidence compiled by Agustina Gallardo (2025) supports this: profit-shifting practices are associated with job losses and reduced bargaining power, while countries with stronger corporate tax systems achieve better employment outcomes and fairer wage distribution. Ending profit shifting is therefore not only about tax fairness but also about ensuring that resources stay where workers are, supporting both decent wages and real investment.

Towards a fairer global tax order

The direction is clear: profits should be taxed where real economic activity takes place. Unitary taxation provides a fairer and more transparent framework to achieve this, ensuring that workers, communities, and public services share in the value created by multinational firms. Combined with a robust global minimum tax, it offers a path to curb avoidance, restore fiscal space, and build a more balanced international tax system.

These findings underline the need for governments and international institutions to build on existing debates and move towards reforms that align taxing rights with real economic substance. A reimagined tax system can close the gap left by profit shifting and deliver more stable revenues to fund decent jobs and public services.

The ongoing negotiations at the United Nations on a Framework Convention on International Tax Cooperation provide a concrete opportunity to advance this shift. Unlike the OECD process, the UN offers every country an equal seat at the table, making it the forum where governments can reimagine global tax rules on fairer terms. If governments are willing to be ambitious, the convention could embed unitary taxation, stronger minimum rates and full transparency at the heart of a new international tax order, thereby ensuring that the revenues linked to real economic activity support jobs, wages, and public services worldwide.